AI Agents for Banking Customer Support: The Complete Guide

Rajni

Last updated on July 13, 2026

AI agents help enterprise banks handle high-volume customer support queries faster across web, mobile, WhatsApp, email, and phone.

From balance checks and KYC updates to loan support, EMI reminders, fraud triage, and smart escalation, AI agents reduce support load while keeping human teams focused on complex cases.

This guide explains the key banking AI agent use cases, benefits, compliance guardrails, and how platforms like YourGPT can help banks build safer, scalable customer support automation.

Banking support has a volume problem. A large bank processes millions of customer interactions every month. A significant portion of them are the same ten questions: balance, transaction history, KYC status, EMI date, loan documents. Individually simple, but at enterprise scale they consume enormous support capacity and still leave customers waiting.

Enterprise support teams are built for judgment calls, disputes, regulatory queries, and high-value customer relationships. Routing a senior agent to answer “what is my available credit limit” at 11 PM is an expensive way to handle a routine request.

That gap is where AI agents fit. Not the old chatbot kind that returns a wall of text when you type “balance” and calls it a day. Actual AI agents that understand what the customer is asking, pull the right answer from approved bank content, follow multi-step workflows across connected systems, and know when to escalate to a human with full context already attached.

For enterprise banks managing support across web, mobile, WhatsApp, and contact centers simultaneously, this is not a convenience upgrade. It is an operational necessity.

This blog covers where AI agents work in banking support, what compliance guardrails matter at scale, and how to build one using YourGPT.

An AI agent is a software system that uses language understanding to handle customer queries end to end. It reads what the customer writes, figures out what they need, finds the right answer or action, and either resolves the issue or routes it to the right person.

In enterprise banking, that means an AI agent handles natural language questions about accounts, loans, KYC, and transactions across thousands of simultaneous conversations. It pulls answers from approved policy documents and FAQs. It connects to core banking systems, CRMs, loan platforms, and ticketing tools. And it detects when a query involves fraud, a complaint, or a situation that needs human review, then escalates with full context already attached.

At enterprise scale, the consistency benefit matters as much as the speed. Every customer in every channel gets the same approved answer. Every escalation follows the same defined rule. Every conversation is logged and auditable.

The core capabilities that drive this are: understanding customer intent without requiring exact phrasing, answering only from content the bank has approved, triggering workflows across connected systems, and routing sensitive or complex cases to the right team without making the customer start over.

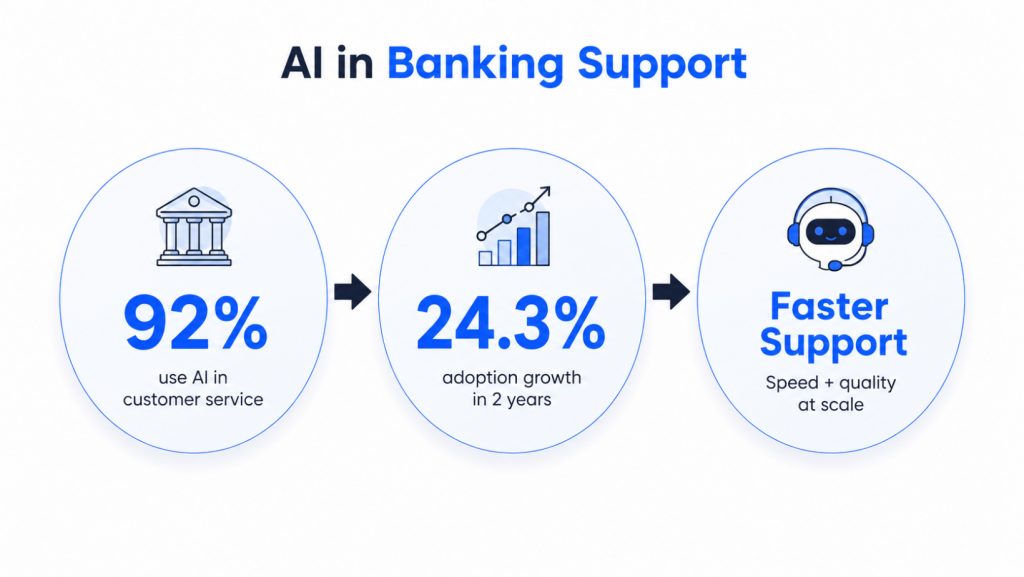

AI adoption in banking support has moved past the pilot stage. Research shows 92% of banking and finance organizations now use AI in their customer service operations, a 24.3% increase in just two years. For enterprise banks, this is no longer a question of whether to adopt. It is a question of how fast and how well.

Three pressures are driving the pace:

Volume – Contact centers at large banks handle millions of queries monthly. Traditional staffing models cannot absorb that load without ballooning costs. AI handles the repetitive tier so human teams can focus on complexity.

Expectations – Customers who get instant answers from retail and tech apps bring those expectations to their bank. Slow, inconsistent support is now a retention risk, not just a satisfaction problem.

Channels – Customers reach out through voice, chat, email, WhatsApp, and mobile apps, often switching between them mid-issue. Building separate teams for each channel is not viable. AI creates a consistent support layer across all of them from a single system.

The banks pulling ahead are not the ones that adopted AI earliest. They are the ones that deployed it with the right guardrails, connected it to the right systems, and kept humans in the loop where it actually matters.

AI agents can improve enterprise banking support by connecting customer requests, internal workflows, and banking systems into a more coordinated service model. Their value is not only in answering queries faster, but in helping banks reduce operational load, apply controls consistently, and scale service across channels while keeping human oversight for sensitive or regulated cases.

For example, see how SKNANB enhanced banking operations with YourGPT AI Chatbot.

The strategic benefit is controlled growth. Capgemini Research Institute reports that 92% of financial services executives surveyed believe AI agents can help firms reach new geographies, while 75% see an opportunity for multilingual support that adapts to local regulations and cultural norms. For enterprise banks, the strongest use case is not replacing human judgment, but combining automation, governance, and human escalation to deliver faster, safer, and more scalable support.

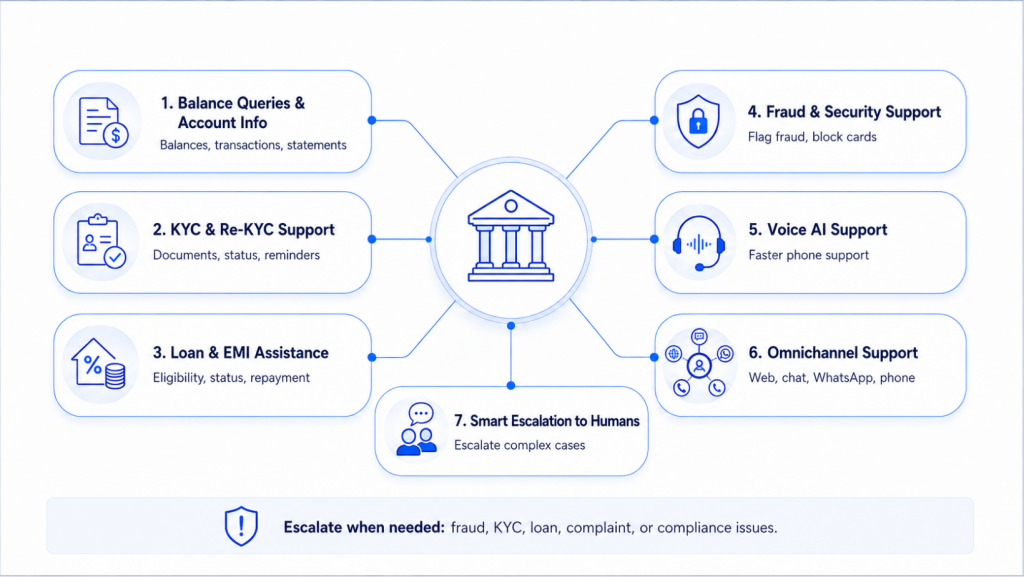

AI agents can handle a wide range of banking support tasks, from answering routine customer questions to assisting with account services and fraud-related inquiries. These use cases help banks deliver faster, more accurate, and always-available customer support.

Balance and account questions are the highest-volume category in enterprise banking support. Tens of thousands come in daily: current balance, recent transactions, deduction explanations, salary credits, credit card limits, and statement requests.

An AI agent verifies identity first, then retrieves the relevant information from connected systems. It explains pending holds or failed transactions and offers next steps, whether that is downloading a statement, raising a dispute, blocking a card, or escalating to a human. At enterprise scale, even a 40% containment rate on these queries frees up substantial agent capacity for fraud, complaints, and relationship work.

Authentication is non-negotiable. The agent must never share account details before OTP, app login, biometric confirmation, or a secure handoff to an authenticated environment. Any setup that skips this creates serious compliance and security risk.

For large banks running re-KYC drives across millions of customers, volume spikes become unmanageable without automation. Customers do not understand which documents are required, why their account is restricted, or what to do after a rejection.

An AI agent covers document requirements, online and video KYC steps, status checks, and missing document reminders. For authenticated customers, it checks live KYC status and raises a ticket when operations review is needed.

Escalation to a compliance or operations team member is required whenever a document does not match bank records, KYC is rejected, an account is frozen, a customer reports a suspicious link, or the case involves a high-risk customer category. These cannot be resolved by an automated answer.

The loan support load spans the full customer lifecycle: eligibility queries from prospects, document questions from applicants, status requests from pending cases, EMI queries from active borrowers, and restructuring or missed payment cases from customers in difficulty.

An AI agent handles the informational layer across all of this. It explains eligibility by product, lists document requirements, shows application status through an integrated loan management system, sends EMI reminders, shares repayment schedules, and raises service requests for prepayment, foreclosure, and NOC issuance. This keeps loan officers focused on credit assessment and high-value client relationships rather than processing fee explanations.

The agent should not promise loan approval, pressure customers toward borrowing, or make credit decisions. Rejection, restructuring, missed EMI follow-ups, and settlement cases all require a human loan officer. The agent collects context, creates a ticket, and hands off.

Fraud queries are the most time-sensitive in banking support. When a customer reports a transaction they did not make, speed matters more than almost anything else.

The agent collects the details, flags the case, blocks the card if requested, and routes to the fraud team with full context. It does not attempt to investigate or resolve the case. Beyond reactive support, AI systems also analyze transaction patterns in real time to flag suspicious activity before the customer notices. According to Deloitte, AI-powered fraud detection reduces false positives by up to 80%, which matters because a wrongly blocked legitimate transaction damages trust just as a missed fraud case does.

A large portion of enterprise banking support still happens over the phone, and traditional IVR systems handle it badly. Customers navigate menu trees, get routed incorrectly, and repeat themselves to multiple agents.

Voice AI replaces rigid menus with conversational interfaces. Customers state what they need, the system understands and responds, and either resolves the query or routes it correctly. It operates at scale without fatigue, handles parallel calls without wait time, and integrates with existing telephony infrastructure so banks do not need to rebuild their contact center stack. For older customers or those in low-connectivity areas, it is also more accessible than app or chat-based support.

Banking customers move between channels mid-issue. A customer might start a loan inquiry on the website, follow up on WhatsApp, and call two days later. Without connected systems, they repeat their story every time.

AI maintains context across all of these interactions. When a customer moves from chat to phone, the conversation history, detected intent, and account context travel with them. The human agent who picks up already knows what happened online. Industry data shows AI-powered chatbots now handle 70 to 85 percent of routine inquiries at 91 percent accuracy. The omnichannel layer is what makes that number meaningful, because the remaining cases reach a human with full context already attached.

The difference between a good AI support setup and a liability often comes down to knowing when to stop and transfer.

In enterprise banking, getting this wrong means a fraud case handled too slowly, a compliance flag missed, or a regulatory complaint that could have been contained. Smart escalation means the agent recognizes when a query needs human judgment and transfers with full context so the customer does not repeat themselves.

The situations that should always trigger escalation:

| Trigger | Example | Team to Route |

|---|---|---|

| Fraud risk | “I did not make this transaction” | Fraud team |

| KYC exception | Document mismatch or rejected KYC | KYC operations |

| Loan issue | Rejection, restructuring, missed EMI, waiver | Loan support |

| Customer frustration | “I have asked this three times already” | Senior support |

| Complaint intent | “I want to file a formal complaint” | Grievance team |

| Low AI confidence | Agent cannot answer accurately | Human agent |

| Regulatory keyword | “RBI,” “Ombudsman,” “legal notice” | Compliance team |

| Vulnerable customer | Elderly customer, language difficulty | Assisted support |

The human agent should receive: customer ID (post-authentication), a conversation summary, detected intent, product involved, issue category, steps already completed, documents checked, a sentiment flag, and a recommended next action. For enterprise contact centers managing hundreds of concurrent queues, this structured handoff is what keeps resolution times and customer satisfaction scores where they need to be.

Implementing AI agents in banking customer support is not only a technology upgrade. It requires the right data, controls, workflows, and human oversight to make automation reliable at enterprise scale.

The safest way to overcome these challenges is to treat AI agents as regulated customer support infrastructure, not as a standalone chatbot project. With the right governance, data readiness, integration plan, and human escalation model, banks can use AI agents to improve support speed while keeping accuracy, trust, and compliance under control.

Enterprise banks operate in a heavily regulated environment. AI in customer support does not sit outside that environment. It sits inside it, and the governance requirements apply in full.

Authentication must precede any account-specific response. Balance, transaction history, card details, and loan data must never appear in an unauthenticated chat window under any circumstances. The knowledge base must contain only compliance-approved content and should go through a formal review cycle, not just an initial upload.

Human review is mandatory for fraud reports, complaint filings, KYC rejections, and loan decisions. The AI agent’s role in these cases is containment and routing, not resolution. Any setup that allows the agent to close these cases unilaterally creates regulatory exposure.

The system needs regular testing for hallucinations, incorrect answers, and edge cases where the agent gives a confident response to a question it should not be handling. Escalation thresholds need periodic review based on actual conversation data, not just initial configuration assumptions.

Role-based access controls apply to anyone who can edit the knowledge base or modify agent behavior. Changes to the knowledge base in a live banking environment should go through an approval workflow, not an open edit.

Clear disclaimers should appear wherever the agent provides loan eligibility information, interest rate guidance, or any content that could be construed as financial advice.

Deploying AI in enterprise banking support requires governance that spans compliance, legal, risk, operations, and technology. The banks that do this well treat the AI agent as a regulated customer touchpoint from day one, not as a technology pilot that gets compliance review later.

AI agents help banks answer common customer questions faster across channels like web chat, mobile apps, WhatsApp, email, and phone support. They can handle routine queries such as balance checks, transaction information, KYC status, loan documents, EMI dates, card issues, and statement requests. This reduces waiting time for customers and allows human agents to focus on fraud, complaints, disputes, and complex banking issues.

AI agents can be safe for banking support when they are built with strong security and compliance controls. They should only access account-specific information after proper authentication, such as OTP, app login, biometric verification, or secure customer validation. They should also use approved banking knowledge, maintain audit logs, follow role-based access controls, and escalate sensitive cases to human teams.

No. AI agents should not replace human support teams completely. Their best role is to handle repetitive and low-complexity queries, while human agents manage cases that need judgment, empathy, regulatory review, or decision-making. Fraud reports, formal complaints, rejected KYC cases, loan restructuring, missed EMI issues, and legal or regulatory concerns should always be routed to human teams.

AI agents are best suited for high-volume, repetitive, and process-driven banking queries. These include account balance questions, transaction status, statement requests, KYC FAQs, re-KYC reminders, loan application status, EMI schedule queries, card blocking assistance, fraud first response, and ticket routing. They work best when the task has clear rules, approved answers, and defined escalation paths.

Banks can reduce incorrect AI responses by training agents only on approved banking content, setting confidence thresholds, testing responses regularly, and reviewing conversation logs. AI agents should not answer questions outside their approved knowledge base or make decisions on loans, fraud claims, KYC exceptions, or complaints. When the agent is unsure, it should escalate the conversation to a human agent with full context.

Enterprise banks face a support problem that scales with their customer base. More customers means more queries, more channels, more complexity, and more pressure on teams that are already stretched across fraud, disputes, complaints, and regulatory obligations.

AI agents address the volume layer of that problem. They handle the questions that come in every day at high frequency and low complexity, consistently and at speed, so that human teams are available for the cases that actually need them.

The use cases that work best at enterprise scale are the ones this guide covers: KYC FAQs, loan support, EMI guidance, account query routing, and structured escalation for fraud, complaints, and regulatory cases. These are well-defined, high-volume problems where automation delivers clear value without compromising the judgment and oversight that banking regulation requires.

With a platform like YourGPT, enterprise banks can build trained AI support agents, connect them to approved knowledge and live banking systems, deploy them across every customer channel, and route sensitive cases to the right human teams with full context intact. The goal is not to replace the people in banking support. It is to make sure they are spending their time on work that only they can do.

YourGPT helps enterprise banks automate high-volume customer support across web, mobile, WhatsApp, email, and phone, while keeping fraud, KYC, loan, and complaint cases routed to the right human teams.

TL;DR Business process automation with AI agents lets software plan multi-step work, call tools, and handle exceptions instead of following fixed scripts like traditional RPA. AI agents can adapt when a process changes, but that flexibility also requires clear permission boundaries, reliable data, and human oversight for consequential actions. Start with one repetitive process, document […]

TL;DR AI web scraping replaces hardcoded selectors with an agent that reads a page, decides what matters, and returns structured output, even after the layout changes. Script-based scraping is being layered with agent-based extraction. Scripts still fetch the page. The model decides what to keep. A fetch layer renders the page, a conversion step strips […]

TL;DR The Shift: Support bots used to answer questions. In 2026, AI agents resolve them by reading live order and carrier data, then taking direct action. They can issue refunds, update addresses, and close WISMO tickets without human involvement. The Stakes: WISMO and refund requests already account for a large share of a typical support […]

TL;DR A customer experience strategy is a documented plan for how people, process, and technology work together across every customer touchpoint, not just a support-team initiative. Strong CX optimization can drive 5 to 10 percent revenue growth and reduce costs by 15 to 25 percent within two to three years, making it an executive-level priority. […]

SaaS companies usually do not hit support overload because the product is failing. They hit it because the product is working. More users mean more onboarding questions, more billing confusion, more integration issues, more feature requests, more account-access problems, and more tickets arriving outside business hours. A small support team that could manage 500 customers […]

TL;DR OpenAI shipped workspace agents inside ChatGPT Business and Enterprise in April 2026, giving the product the ability to plan multi-step work and act inside connected tools. The update narrows the gap between ChatGPT and dedicated AI agents for internal work, but it does not replace customer-facing support platforms. Workspace agents live in the ChatGPT […]